It’s a rapidly evolving pet economy where services, expertise, and experience drive the next wave of growth.

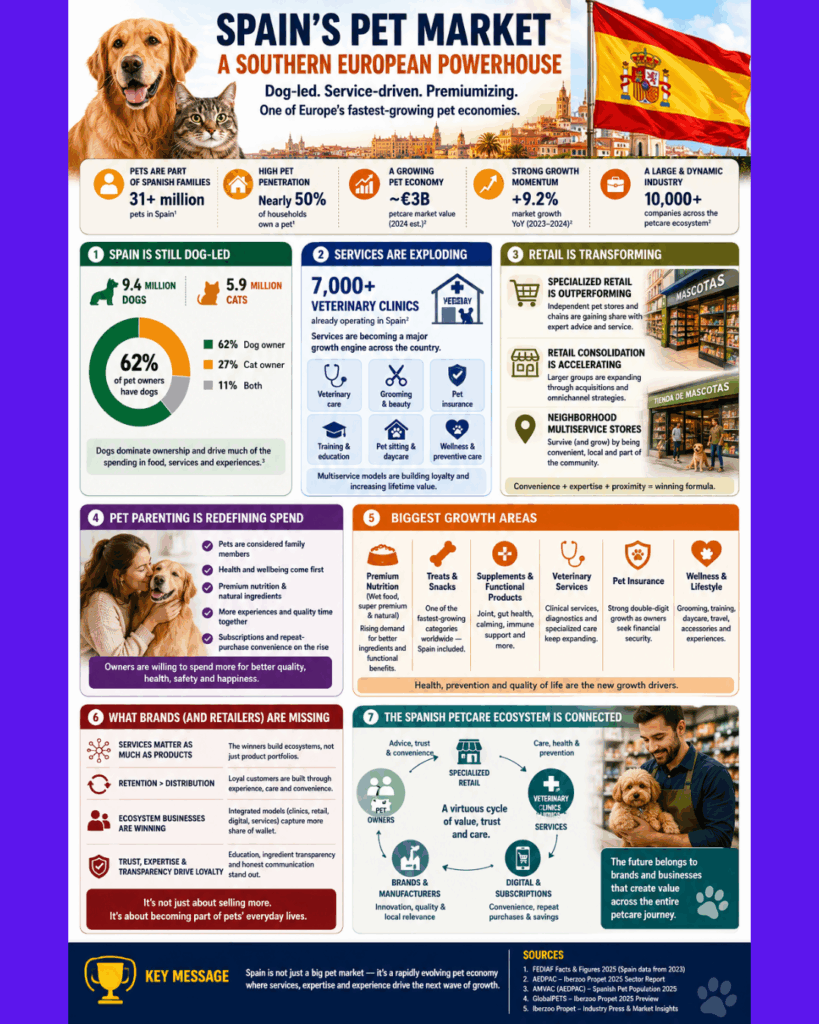

Nearly 50% of households in Spain own a pet, and pets are a big part of Spanish families, counting over 31 million pets.

According to the latest FEDIAF 2025 data (based on 2023 population figures) Spain has about:

→ 9.4M dogs vs 5.9M cats

→ 62% of Spanish households own at least one dog

→ 27% of Spaniards own at least one cat

→ 11% of Spanish households have both

That makes Spain one of Europe’s largest dog markets, not a cat-led market, unlike the Nordic countries or Germany.

Dogs still dominate ownership and services, while premiumisation is reshaping spending behaviour across categories.

The most interesting part is that the pet economy, which is ~3B€, points Spain as one of Europe’s fastest-growing petcare industries:

▪️Petcare sector growing ~9.2% YoY

▪️10,000+ companies operate in the ecosystem

▪️7,000+ clinics already active

▪️Services are becoming a major revenue engine

▪️Retail consolidation and multiservice pet stores are accelerating

▪️Veterinary, grooming, insurance, and wellness are expanding fast

▪️Pet parenting is reshaping spending behaviour

▪️Specialised retail is outperforming traditional channels

Pet parenting is changing in behaviour,

Millennials and Gen Z are looking for:

– Premium nutrition

– Health-first spending

– Subscriptions and convenience are rising

And these are what brands seem to still be missing:

👉🏽 Services matter as much as products

👉🏽 Retention > distribution

👉🏽 Ecosystem businesses are winning

👉🏽 Trust and expertise drive loyalty

The brands adapting early will likely capture the highest-margin segments first 🧡

Sources: FEDIAF, The European Pet Food Industry, AEDPAC and GlobalPETS

LinkedIn original post: https://www.linkedin.com/posts/angels-bosch