I keep on reading two opposite things about our relationship with pets and money.

We are facing a record in pet spending and a record in “Petflation”.

At once.

Something doesn’t add up, right?

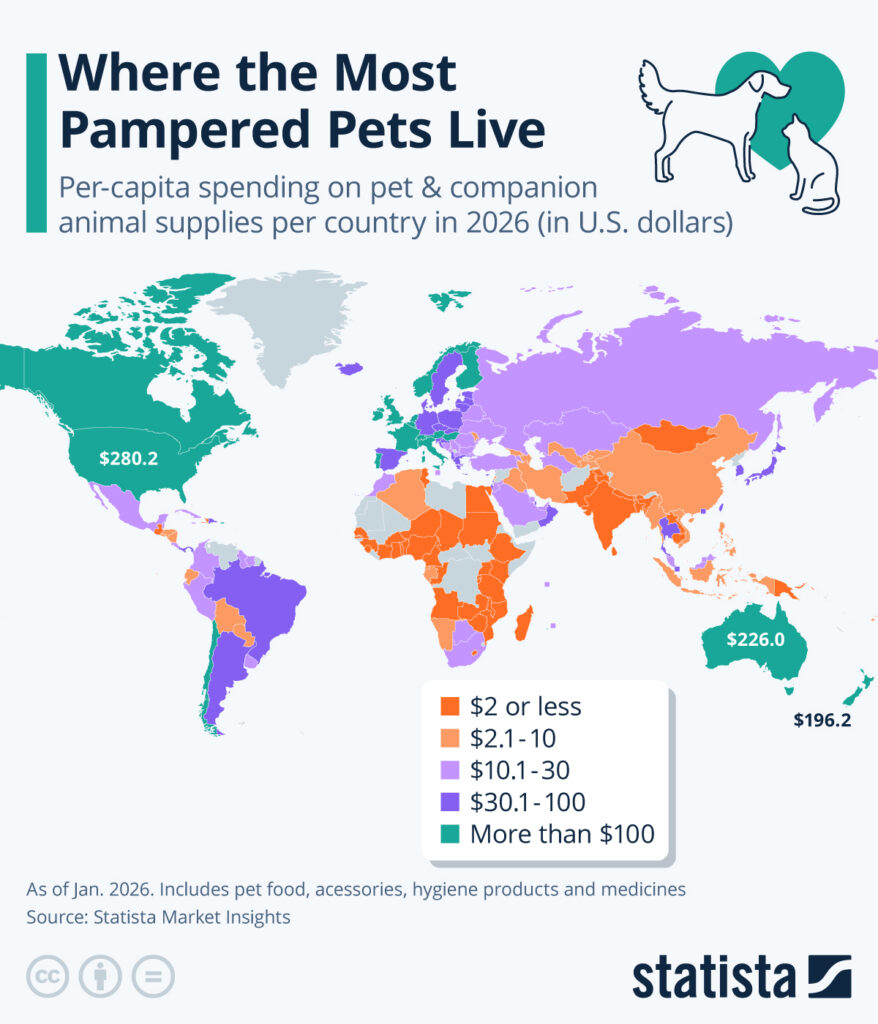

1️⃣ The US is now the world’s most “premium forward” pet nation

Americans are on track to spend ~$280 per capita on pet supplies in 2026, followed by Australia and New Zealand. While in Europe, Portugal and Finland spend disproportionately more on pets compared to their income levels.

The “pets as family” mindset remains strongest in North America, Western Europe, and parts of Latin America. While much of Asia and Eastern Europe represent future growth potential.

2️⃣ Total “petflation” hit 3.4% year-over-year in January (42% above the national U.S. inflation rate), extraordinarily in vet services (7.4%) with pet prices now 33% above pre-pandemic levels.

Pet spending is recession-resistant but not inflation-proof.

→ For the industry, the numbers are broadly positive. The market is massive, growing, and remarkably resilient.

→ For consumers, the picture is more mixed. It may be forcing some difficult choices between quality of care versus affordability.

The brands that win in this environment won’t just sell products.

Value positioning matters more than ever.

Premium must justify itself.

Reassurance is becoming as important as aspiration.

Are you positioning your brand for the value-conscious pet parent or are you still marketing to 2019?